Credit commons - introduction

“If the entire world gets a decentralised financial system with inter-connected mutual credits, I think that could be amazingly beautiful, and move us past this ‘Stage 1 Civilisation’ where we actually start to look at what we want to do as humans, rather than just make money.” – Will Ruddick, Grassroots Economics

Contents

What’s a credit commons?

It’s the ‘money system’ for the commons economy, if you like. Money in the modern world is credit, and from a commons perspective, that credit should belong to all of us, in common, not the banking system. Thomas Greco coined the term credit commons to describe a global system of mutual credit networks linked via a protocol.

A mutual credit trading network in any town can be seen as that town’s credit commons. So, for example in Bristol, a city-wide mutual credit network could be called Bristol Credit Commons, where credit is held in common – just as housing is held in common in Bristol Housing Commons.

A global credit commons can be built by federating local trading groups together (but with autonomy for local groups), and the tool for doing that is the Credit Commons Protocol (see below). So we can talk about credit commons as a concept, but use capital letters when we talk about a town’s network, the global network or the protocol.

Global Credit Commons

We need scale to challenge the current money system, but starting at scale involves massive cost and risk (of failure or corporate takeover). Credit commons is about federating small, local schemes to get to scale.

The global Credit Commons concept is like the Internet – something that we can all plug into. It can incorporate business networks that trade with each other using mutual credit, fiat, crypto or barter, or anything else. But their relationship with the rest of the CC will be a mutual credit relationship.

Elinor Ostrom, in Governing the Commons, suggested that to grow, commons should be ‘organised in multiple layers of nested enterprises’, which is exactly what the CC does, in a recursive, fractal way, like sociocracy, but for trade rather than governance.

Credit Commons Protocol

Matthew Slater and Tim Jenkin introduced the Credit Commons Protocol via a White Paper in 2016. It’s a set of standards and rules that govern how transactions are recorded and managed within a network. It utilises digital ledgers, similar to blockchain, to ensure transparency, security, and accountability. However, it differs from blockchain in emphasising mutual credit rather than cryptocurrencies.

A protocol is a bit like the rules of chess. To exchange with each other, we have to agree about how we keep score, otherwise there’ll be free-riding, disagreements etc. With chess, if someone has a different idea about what chess is, you’re not going to be able to play with them.

The Protocol doesn’t just keep track of balances, it checks members’ balance limits, and prevents transactions that violate those limits. So you don’t just need trust and collaboration, you need balanced trade within the network, to allow members to buy and sell without becoming stuck at their limits.

Mutual credit is based on trust – which doesn’t scale. So previous mutual credit schemes had to stay small, trust-based and genuinely mutual, but without the economic diversity for widespread change. Or they go the way of the Wir Bank in Switzerland (it was formed as a mutual credit scheme about 100 years ago). They got big (about 1% of Swiss GDP) – but to scale up, they massively centralised, and now it’s more like a private currency, run by a bank. The choice was to stay small and mutual, with negligible impact, or have a big impact, but lose mutuality. The point of the Credit Commons Protocol is that you can achieve both scale and decentralisation through recursive federation. Without the CC Protocol, as mutual credit networks grow, they can become centralised, and then vulnerable to buyout by venture capitalists.

This article explains the CC Protocol in more detail.

What are the benefits of credit commons?

- Democracy: it’s clear from the name that the means of exchange is credit (a relationship) rather than a commodity or token (a thing), that can be hoarded, accumulated and lent at interest, which concentrates wealth, creating inequality and preventing real democracy.

- Community: credit commons is inherently community-based, and thrives on trust and cooperation. Communities can be geographical or based on shared interests and goals. Communities get control over their own economies, fostering trust and co-operation and a culture of mutual aid.

- Transparency: each group has its own ledger to record all transactions, that’s accessible to all members, ensuring transparency and reducing the risk of fraud. Each community or network maintains its own ledger, and multiple communities can connect their ledgers to form larger networks.

- Poverty: transactions don’t require traditional money – great for communities with little money (this doesn’t mean that things are free of course, it just means that in effect, you pay for things with your work, rather than with money). It also removes the need for interest – which should make things cheaper (Magrit Kennedy estimated the interest proportion of prices of consumer goods to be around 50%!). Also, rich countries export more goods to poor countries than they buy back, so poor countries run out of money, then fall into debt and servitude. That can’t happen in a system where the surplus and deficit partners work together to balance trade rather than accumulating money or debt. That’s why Keynes wanted a global mutual credit system instead of the IMF after World War II.

- Resilience: communities are less dependent on external financial systems and can continue trading even during economic downturns or crises.

- Accessibility: accessible to anyone with the necessary technology, making it an inclusive alternative to traditional financial systems; particularly beneficial in marginalised communities.

- Environment: promotes local trade, because each network will probably charge a tiny transaction fee to cover costs, so fees will be slightly higher the further apart the parties in a transaction are (i.e. the more ‘layers’ the trade has to pass through). This gives an incentive to look more locally for what you need, so shortening supply chains.

- Freedom from bankers: the credit commons could replace money (credit issued by banks) with credit that we issue ourselves, which means no interest, no monopoly on credit creation, and no banks required!

What can I do?

The main route to a global Credit Commons is via credit clearing and mutual credit – tools that can be used by networks of trading businesses. Credit clearing networks are growing in places like Liverpool, in ways that will be replicated everywhere. Local mutual credit networks can be generated from clearing schemes, or started by a group of small businesses that trade with each other regularly. Contact us if you’re part of a group that may be interested, and we’ll put you in touch with specialists who can help.

The system has 2 layers – the protocol and the implementation (specific local agreements layered onto the protocol). Implementations can be unique and varied, as long as they speak the language of the protocol, so different groups can interact.

The CC Protocol is ‘open source‘ – anyone can use it freely. If you understand open-sourced code, you can see the documentation and repository on GitLab (which includes ways to ask for help if you get stuck).

Each local group will have a ‘front end’ – an app for users, which can be unique, set up for local needs, that interacts with the (‘back end’) that does nothing but implement the shared Protocol.

The ‘front end’ and ‘back end’ need to interact – i.e. instructions from users need to be certified as conforming to the Protocol. This requires an API, which exists, and is again, free and open-sourced, available via GitLab. This allows programmers to write their own implementations (back-end or front-end), confident that their code can interact with other CC implementations. And everything is interoperable with existing accounting packages.

Payments: imagine the global network as a tree, and businesses as leaves. A payment from leaf A to leaf B travels up a twig to a small branch etc, towards the main trunk, until it comes to the first common branch, from where it travels down smaller branches and twigs to leaf B.

Technologically-inclined people can contribute by developing and improving the software and platforms that support the Credit Commons, including creating user-friendly interfaces, enhancing security features, and ensuring interoperability with other systems. Contact us if this might be you.

Credit commons and the commons economy

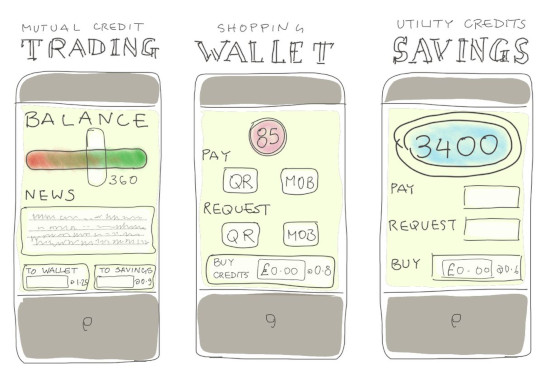

Tom Woodroof of MCS and Local Loop Merseyside explained how various aspects of the commons economy can be connected via the CC Protocol: “the vision is that you’ll have a wallet app on your phone. If you’re a business, you can add your invoices so that you can do credit clearing. You’re also part of a mutual credit network within that larger clearing network, so you have a mutual credit balance. In other parts of your life, you’re a consumer, so you have a balance showing how many local retail vouchers you have, and then you also have a balance that shows your rent credit obligations as a tenant of the local housing commons or your energy vouchers in the local energy commons. This will be one app with different modules/accounts, all interoperable“.

Credit Commons Society

The Credit Commons Society (CCS) has been set up to to foster an ecosystem of groups and networks supporting the Credit Commons, and will be involved in its governance. You don’t want the same people running the system and providing governance oversight. A body with experienced ‘elders’ will provide governance. It’s intended to function as a foundation (like the Linux Foundation, for example, or in the case of the chess analogy above, like the World Chess Federation), helping build a global Credit-Commons-enabled economy.

Further resources

- Tom Greco, the End of Money and the Future of Civilisation

- Credit Commons Protocol

- Credit Commons Society

- Credit Commons documentation and repository on GitLab

We’ll provide more info in future blog articles, which we’ll link to from here.

Specialist(s)

Thanks to Dil Green, Matthew Slater and Tom Woodroof for information.

The specialist(s) below will respond to queries on this topic. Please comment in the box at the bottom of the page.

Dil Green was an architect and builder for 30 years, working on projects from an extension to London’s Science Museum to an award-wining eco-surgery. He now works away at systemic leverage points around Governance, Wisdom: Pattern Language, and Economy: Mutual Credit Services. He lives in Brixton, and blogs at digital-anthropology.

Matthew Slater develops software for complementary currencies. He co-founded Community Forge, which free hosts software for collaborative credit schemes; he co-authored the Money & Society MOOC, a free masters level multidisciplinary online course. He co-drafted the Credit Commons white paper.

Tom Woodroof is in the core team at Mutual Credit Services and Local Loop Merseyside, and convenes the Circular Trade Analytics forum. He has a PhD in applied nuclear physics from the University of Liverpool.